The keyword for markets going forward is instability.

Following Tuesday’s unexpectedly higher CPI numbers, the market has been forced to abandon its hope for a quick end to inflation and a Fed pivot.

Instead markets must confront the following:

Inflation that is going to be higher for longer.

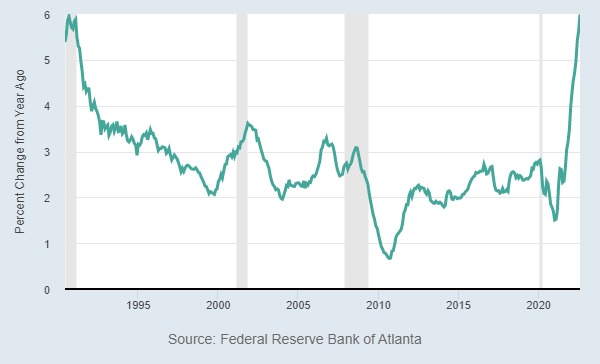

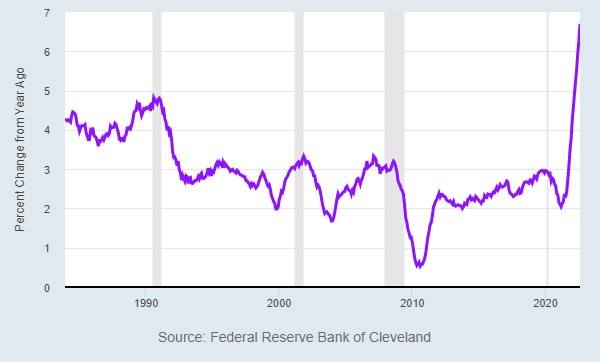

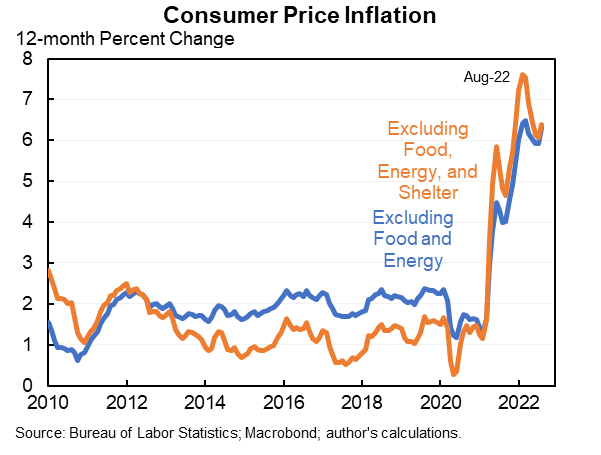

Most tellingly, the inflation measures most representative of entrenched inflation (Core CPI, Median and Trimmed Mean CPI, and Sticky CPI) are not showing any signs of slowing down (see charts below).

Outside of gasoline, food prices affect consumers most and food prices are not moderating. Food inflation was up +11.5% and grocery inflation is running at +13.5% year-over-year (highest since 1979).

A Federal Reserve that is laser-focused on defeating inflation.

The Fed is not going to pivot anytime soon.

As Chairman Powell stated at Jackson Hole, they are willing to take “forceful and rapid steps to moderate demand.”

Higher interest rates until prices moderate enough to satisfy the Fed.

More rate hikes are on the way as the terminal Fed Funds rate may need to be even higher in order to effectively curb demand (see chart below).

Slower demand means a slowing economy means reduced earnings.

A recession may be needed to stop stubborn inflation.

Investors must be prepared for such a recession/slowdown to show up in a company’s bottom lines.

This makes for an unstable, uncertain market.

There are few catalysts to buy when the market is staring down the barrel of the inevitable: a forced economic contraction that might, we hope, stabilize prices.

KEY TAKEAWAYS

Slowdown arriving soon? Atlanta Fed’s most recent estimate for Q3 GDP growth falls to 0.5%.

The certainties for this economy (higher rates, falling demand) make for an uncertain stock market.

Uncertainty for stocks means volatility.

Further whipsaws, bear market rallies, and high magnitude intra and interday moves are to be expected in the coming months.

We are seeing further defensive tactical allocations to cash and cash-like instruments as a way to approach this trendless market.

MARKET CHARTS

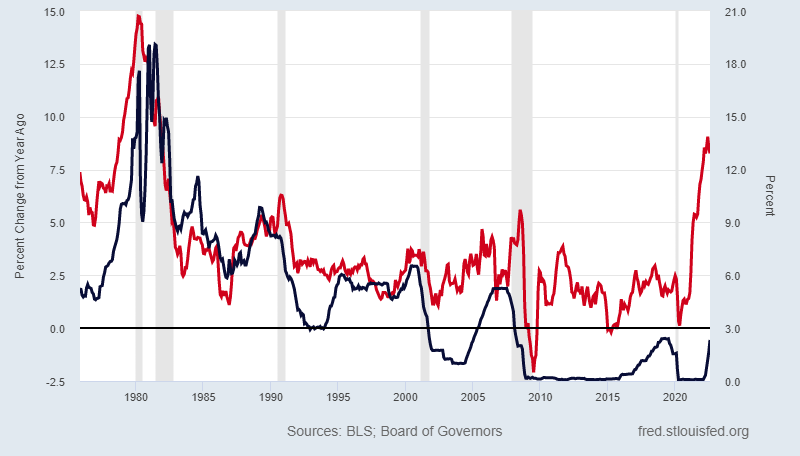

EXHIBIT 1 - Inflation and the fed funds rate

Here we see the rate of inflation (red line) and the effective Fed Funds Rate (blue line). Hiking the Fed Funds Rate is a key part of how the Fed is trying to bring inflation down.

You can see how low the rate remains even after the hikes so far this year. Does this imply the rate needs to be much higher to pull inflation down?

EXHIBIT 2 - fed isn’t budging from being “forceful and rapid” in their hikes

Sticky CPI: highest since ’82, no signs of slowing down.

Median CPI: highest ever recorded (index started in ’83), not slowing.

Core Core CPI: excludes food, energy and shelter, still above 6%.

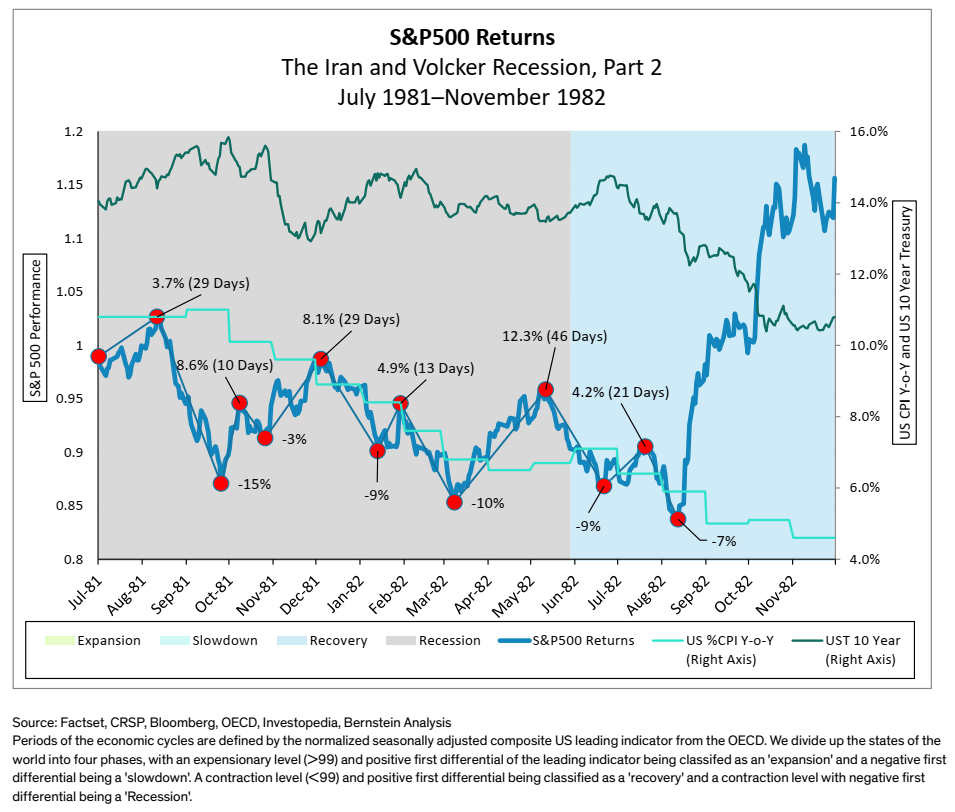

EXHIBIT 3 - Stock returns and last inflationary regime

During our last bout of elevated inflation and rising interest rates stocks didn’t bottom until over two years after the peak in inflation. In between? Sideways movement with whipsaws and bear market rallies.

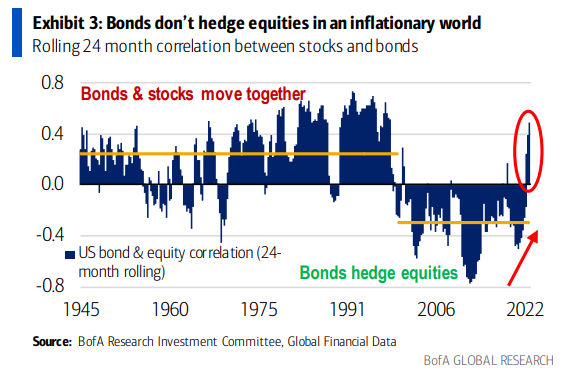

EXHIBIT 4 - bonds don't hedge equities in inflationary world

The views expressed above reflect the views of EdgeTech Analytics, LLC and are for informational purposes only. These views are not intended to serve as a substitute for personalized investment advice. Past performance is no guarantee of future results and no investment strategy or methodology can guarantee profits or protect against losses.