The market has been optimistic about equities this month.

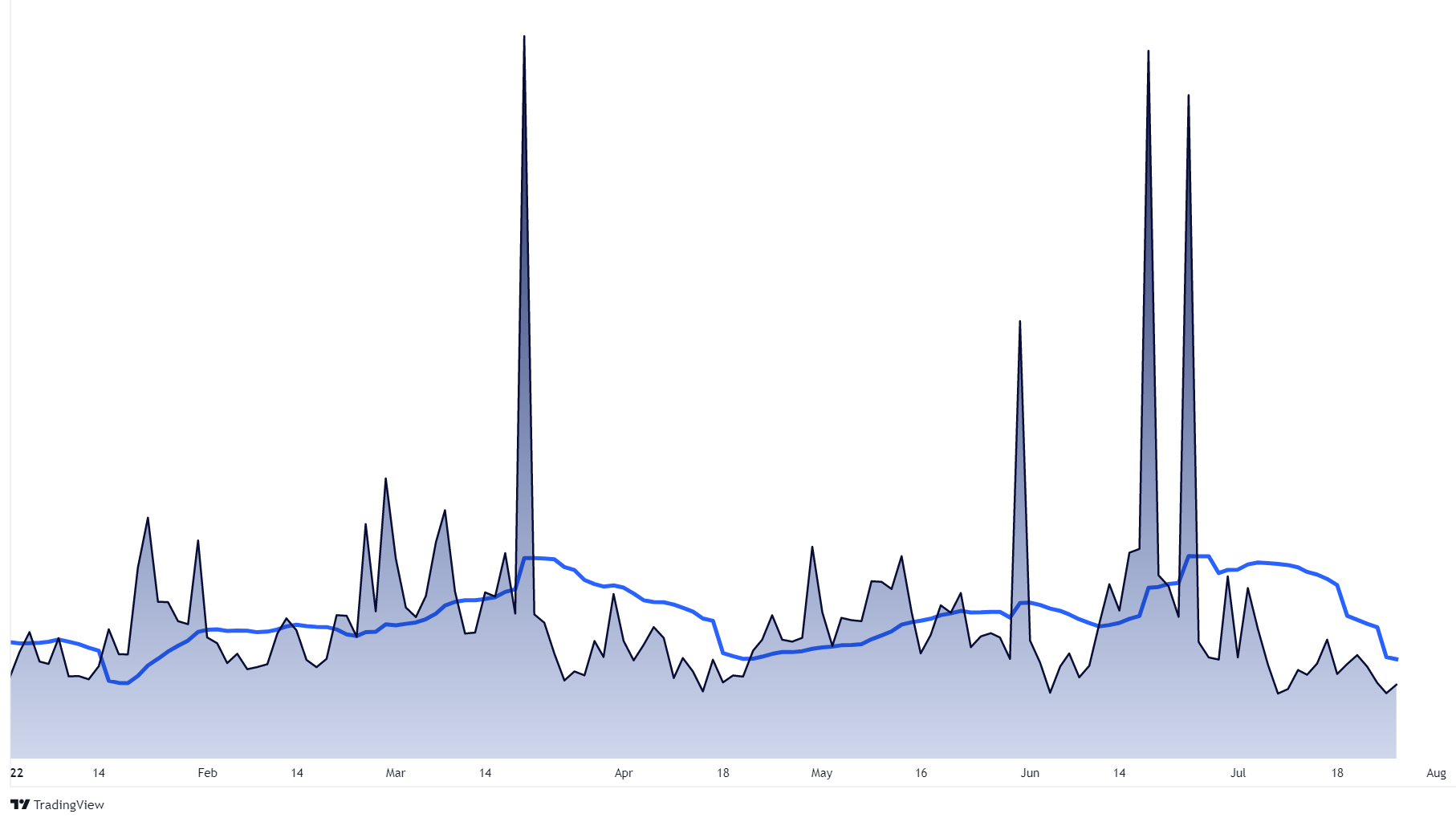

July has been the market’s calmest month volatility-wise, and it has been quiet in terms of active trading (volume).

In a week where we both entered a technical recession (2 consecutive quarters of economic contraction) and the Fed hiked interest rates another 0.75%, stocks shrugging these conditions off does not appear to us to be based on any valid, stable market narrative.

In a week where we both entered a technical recession (2 consecutive quarters of economic contraction) and the Fed hiked interest rates another 0.75%, stocks shrugging these conditions off does not appear to us to be based on any valid, stable market narrative.

The market is forward-looking and its current assessment of the second half—its sanguine view of the chances of a soft-landing (avoiding recession), the reduction in inflation, and the Fed’s dovishness—does not track with the data we’ve been observing this week.

Inflation remains high and the Fed has not minced words about devoting all of their attention to beating it regardless of whether or not this pushes us deeper into recession.

We are concentrating on the market filters in portfolios to help us determine the strength and durability of this latest rally.

We will also be deploying the bench to increase the number of assets, increase the number of check dates, and therefore increase the number of overall opportunities to reenter this market as lasting trends are uncovered.

This has been a frustrating stair-step rally with more ups than downs so far and with disappointing volume. Conviction, therefore, may be lacking.

Our tactical positions stand prepared to deploy should conviction strengthen and trends sustain upward momentum.

NYSE Total Volume - 20-day Moving Average

Back to January levels.

MARKET CHARTS

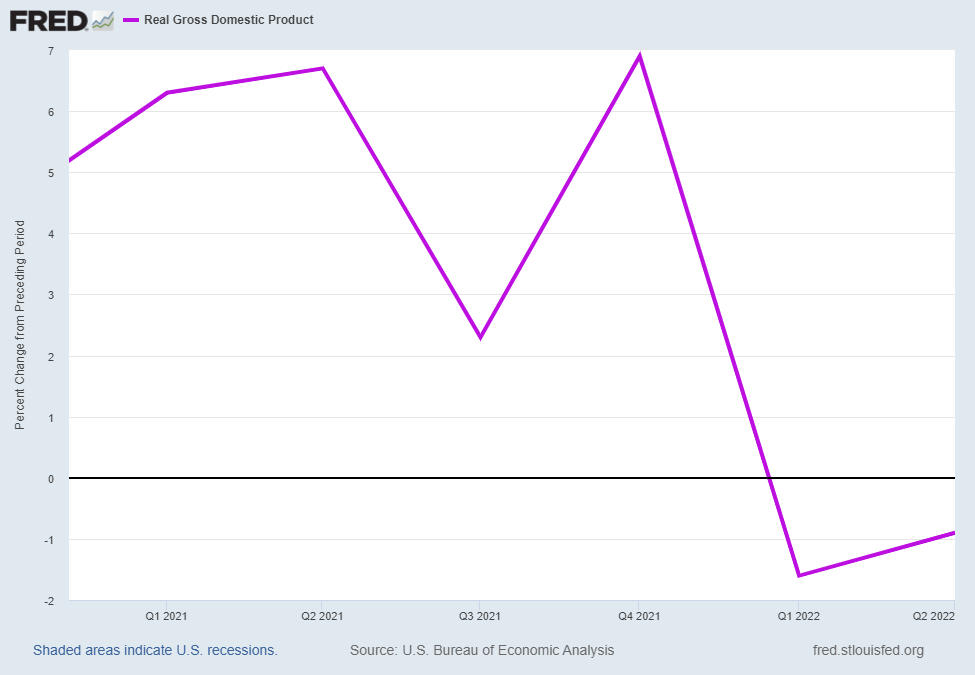

EXHIBIT 1 — U.S. Economy Enters Technical Recession

GDP growth contracted -0.9% in the second quarter; its second consecutive contraction.

The last time we had two quarters of contraction that wasn’t considered a recession was 1947.

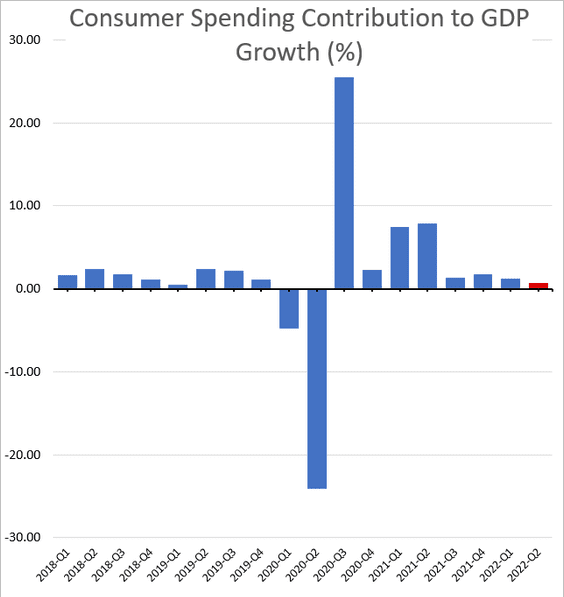

At left we see consumer spending contracting thanks to inflationary pressures such that it is contributing less to GDP.

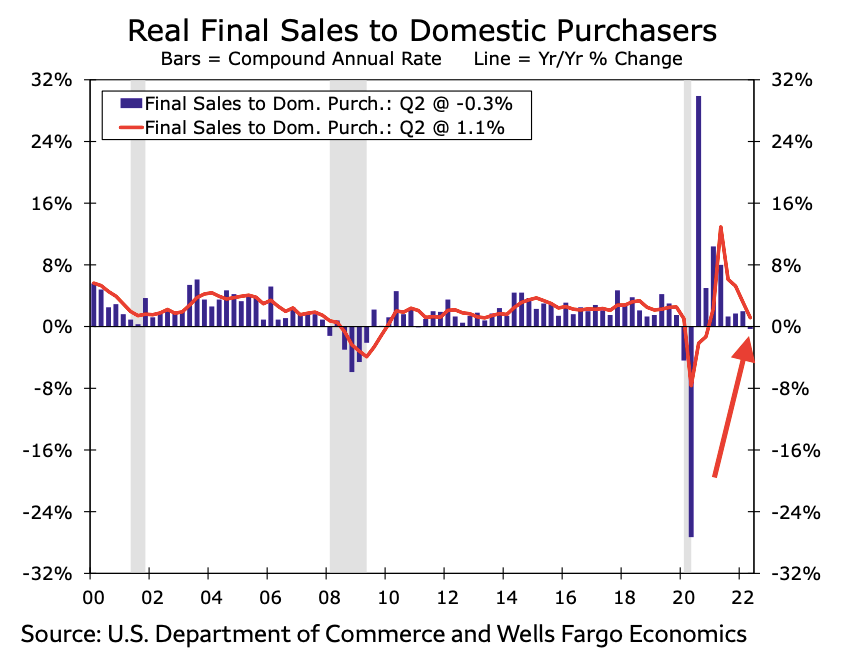

At right we see “Real Final Sales” which is an excellent measure of demand that strips out exports and inventories from the GDP calculation. This shows that real final sales contracted last quarter for the first time since Covid; and before that the last time it contracted was the Great Financial Crisis.

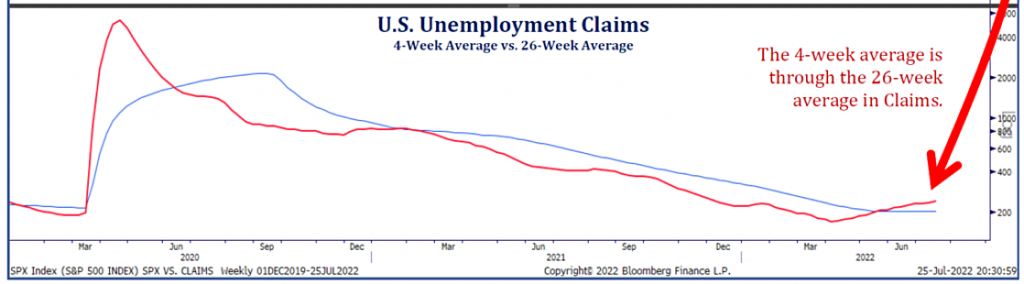

EXHIBIT 4 — Unemployment Claims on Upswing

At left we see consumer spending contracting thanks to inflationary pressures such that it is contributing less to GDP.

At right we see “Real Final Sales” which is an excellent measure of demand that strips out exports and inventories from the GDP calculation. This shows that real final sales contracted last quarter for the first time since Covid; and before that the last time it contracted was the Great Financial Crisis.