As was expected, the Fed hiked short-term rates 75 basis points for the 4th time in a row yesterday.

The Fed Funds rate now ranges between 3.75 – 4%.

As was somehow not expected (based on the two week wishful thinking rally in stocks), Chairman Jerome Powell reiterated the stance he’s taken since they started hiking rates: hawkish and determined to defeat inflation no matter what happens to the economy or markets.

Powell acknowledged that monetary policy takes time to show up in the economy (lagging effects), though he also stressed that we are far from ending the fight against inflation. He stated loud and clear so that the stock market could hear:

“It is very premature to think about pausing.”

“We have a ways to go. I would want people to understand our committment to getting this done.”

“We have some ground left to cover…and cover it we will.”

Powell urged, in as clear terms as he could muster, the stock market to consider the reality of the moment:

Inflation remains stubbornly high.

Core PCE (their preferred measure) has risen for 2 straight months and sits at 5.1%.

Core CPI has also risen 2 straight months and sits at a very high 6.7%.

The economy is not slowing enough to cool inflation to the degree the Fed needs it to.

The ISM Manufacturing PMI index came in above expectations this month and remains at expansion levels (50.2).

The Atlanta Fed is estimating Q4 GDP to come in at 3.6%. An acceleration over Q3 thanks to real consumer spending continuing to rise.

The labor market remains very strong and is a key indicator the Fed is watching when it comes to inflation. As Powell stated in September, “We need to have softer labor market conditions.”

The JOLTS job openings report this week came in a full million more than expected!

As it stands this week, there are 1.9 job openings for every unemployed American. This is nowhere near a weak labor market.

October jobs numbers come in tomorrow. (ADP numbers came in 54k over expectations).

Large cap tech hurt most:

The S&P 500 is down about -22% from its peak (it bottomed at -25%).

The Nasdaq is -35.2% away from peak though it is approaching a new bottom (it’s just 80 points away).

The Dow has been buffeted by its Financials, Healthcare, and Industrials components and is outperforming other major indexes. It’s down -12.5% from peak.

The Dow, like the S&P 500, has met with resistance at its 200-day moving average (see charts below).

MARKET CHARTS

EXHIBIT 1 - S&P 500 and Dow find resistance at 200-day moving average

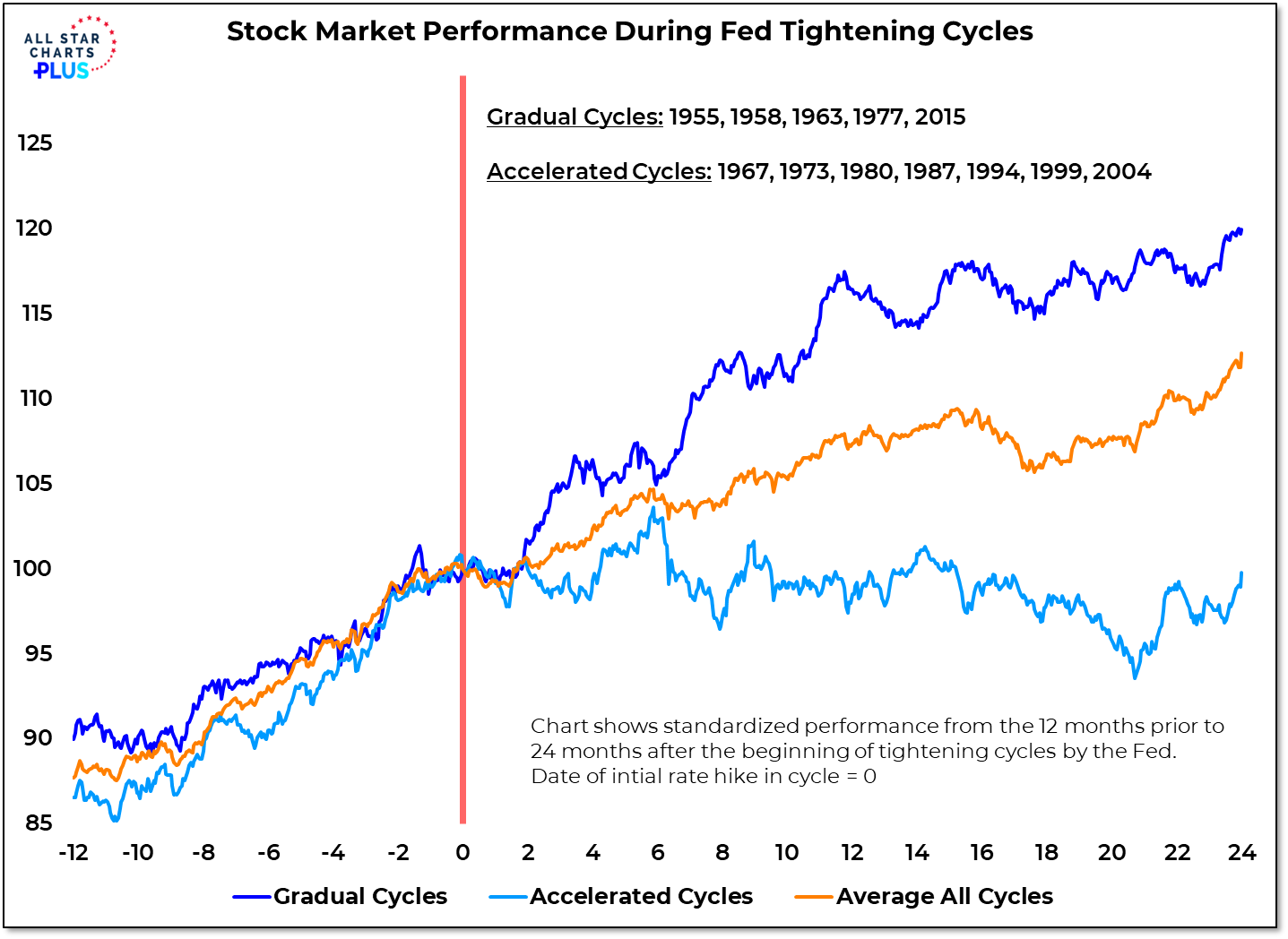

EXHIBIT 2 - fast tightening cycles hurt equity performance

Fast tightening cycles, particularly those to combat inflation, lead to flat equity performance.

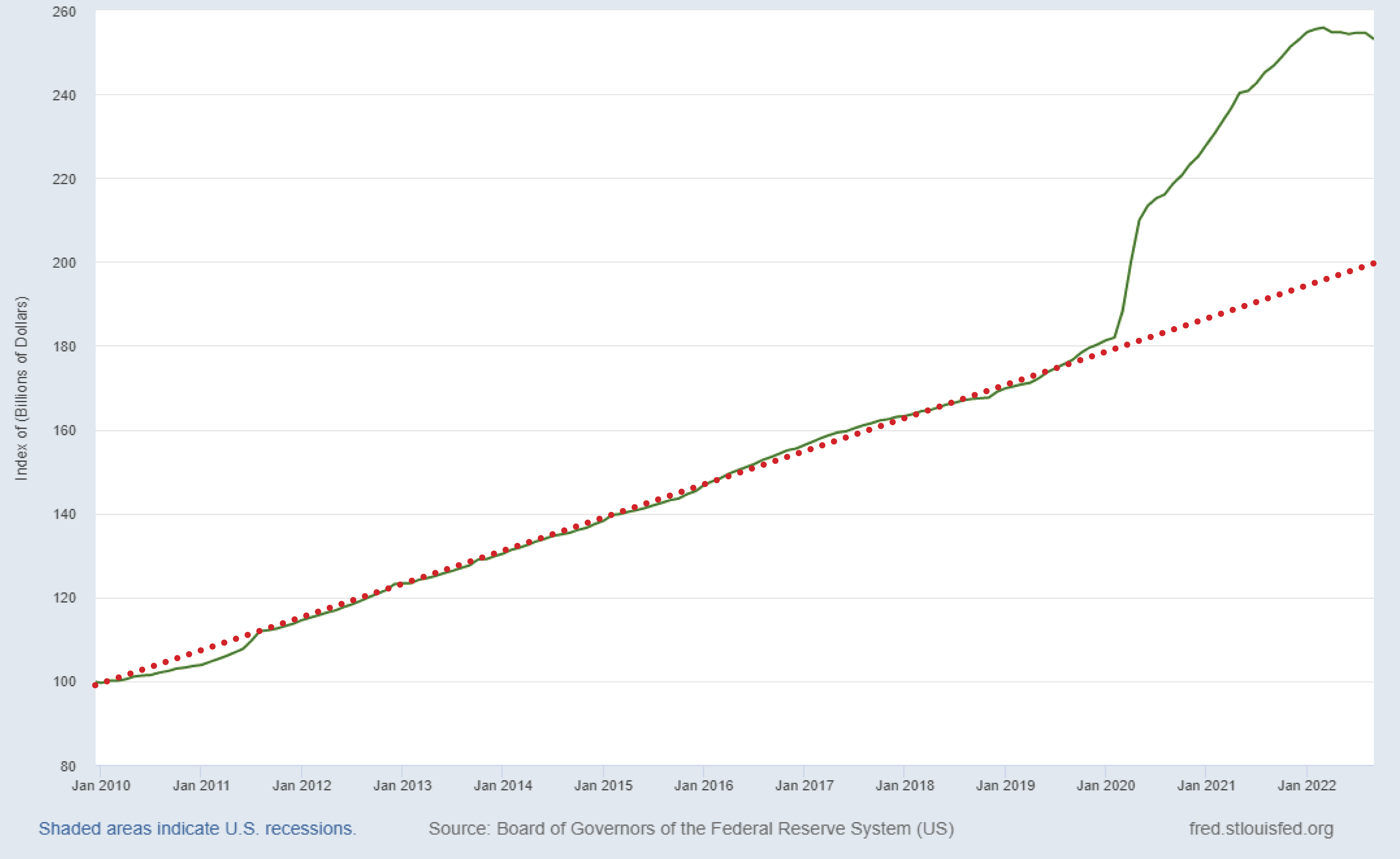

EXHIBIT 3 - why inflation? check money supply

Here we see the amount of M2 money supply (the green line). Notice the jump in 2020 thanks to the trillions in stimulus that went direct to consumers, businesses, and local governments.

The amount is starting to come down, but we are still far from the normal trend line (red dots).

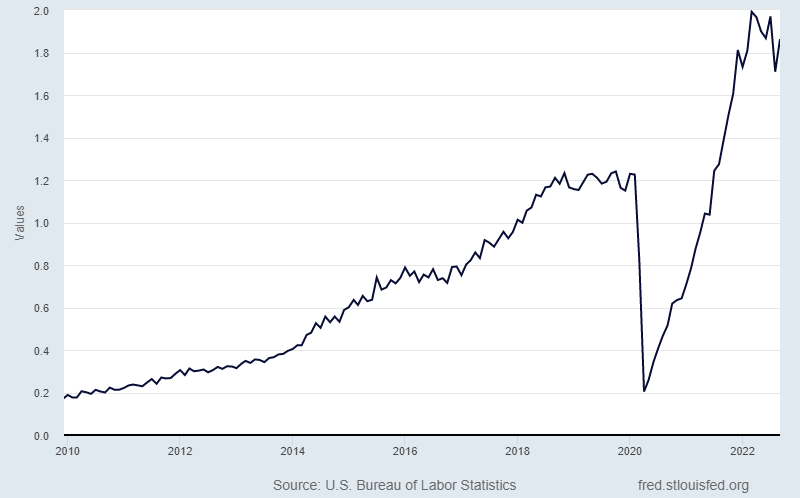

EXHIBIT 4 - job vacancies to unemployed ratio remains elevated

This chart shows the ratio of job openings (vacancies) the the amount of unemployed in the economy. As you can see the number went up last month and sits at 1.8 jobs vacant/open to every unemployed American.

The views expressed above reflect the views of EdgeTech Analytics, LLC and are for informational purposes only. These views are not intended to serve as a substitute for personalized investment advice. Past performance is no guarantee of future results and no investment strategy or methodology can guarantee profits or protect against losses.