The stock market is now confronting the unavoidable: entrenched inflation and a Fed Chairman ready and willing to be the next Paul Volcker.

In this unusual post-pandemic macro environment the Fed’s dual mandate—full employment and stable prices—are in direct conflict.

With the employment rate at just 3.7% the Fed has made the correct judgment call that defeating inflation should be their primary focus for the foreseeable future.

As Chairman Powell stated, a failure to tame inflation with current economic pain would only lead to far greater pain in the future.

And so stocks have seen extreme volatility and have sold off about -10% since the Jackson Hole speech.

Stocks sold off on yesterday’s 75 basis point hike and Powell’s hawkish comments in his afternoon press conference. Some choice quotes:

“It would be nice if there was a way to just wish it [inflation] away, but there isn’t.”

“We think we need to have softer labor market conditions.” I.e., the Fed is willing to tolerate higher unemployment.

“We have got to get inflation behind us. I wish there were a painless way to do that; there isn’t.”

The S&P has again fallen -20% from its peak and the Nasdaq has again fallen -30% from its peak. Both last saw these low levels in July before the summer bear market rally.

Just 15% of S&P 500 stocks are trading above their 50-day moving average; just 10% of Nasdaq 100 stocks are.

KEY TAKEAWAYS

The Fed seems to have given up hope of a “soft landing” and admit economic pain will likely be a necessity to bring inflation down.

Rates are going to continue higher until the Fed sees “compelling” evidence that inflation is moving in the right direction.

What consitutes “compelling” we can’t know, but this uncertainty ushers in volatility in anticipation of every inflation-related data release.

Also, the certainty of higher rates ensures the continued presence of a massive headwind for stock prices.

Such erratic markets facing certain, known headwinds makes for an extremely difficult trading environment. Tactical, defensive allocations to cash and cash-like instruments will be helpful in avoiding catching a knife that’s both falling and bouncing around.

MARKET CHARTS

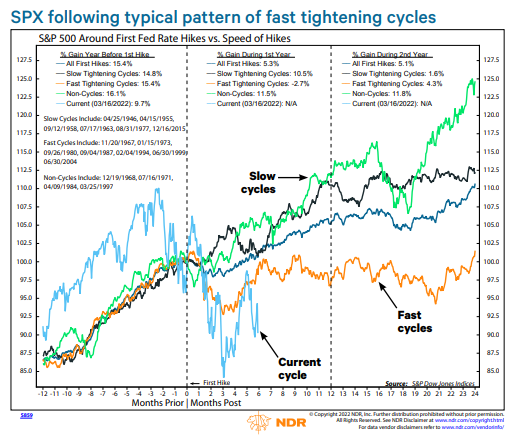

EXHIBIT 1 - Fast rate-tightening cycles leads to disappointing returns

This chart from Ned Davis Research shows S&P 500 performance during different speed rate-tightening cycles.

Fast hiking/tightening leads to volatile, flat performance historically.

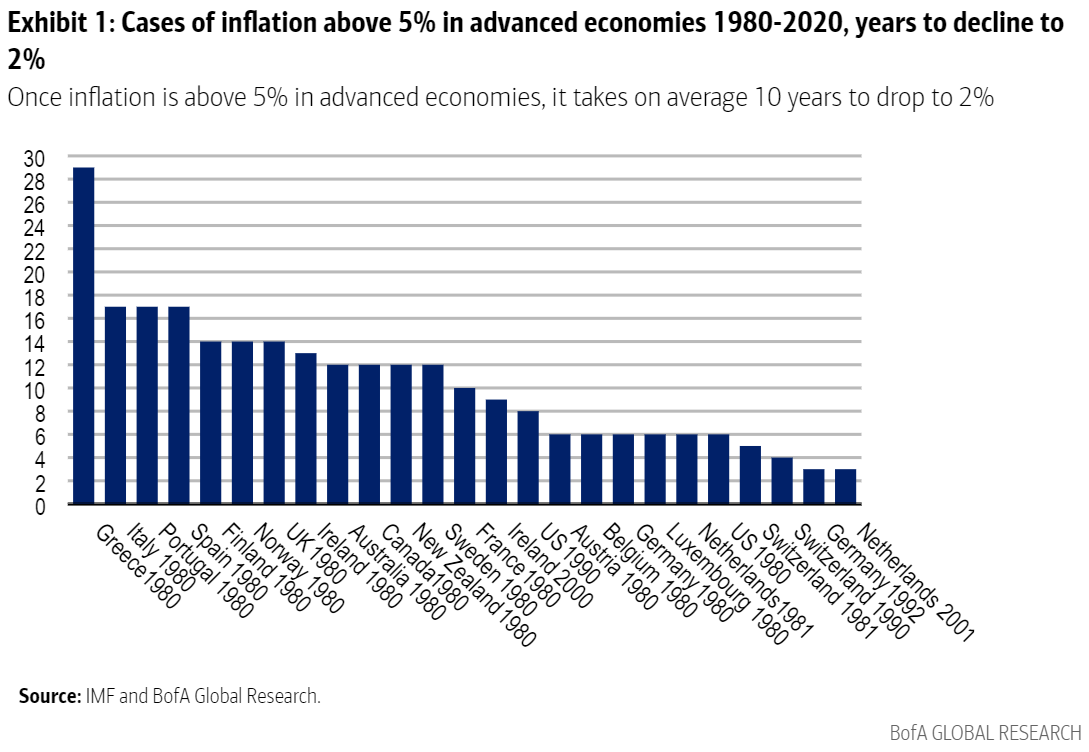

EXHIBIT 2 - how long to kill inflation?

Research from Bank of America shows that in advanced economies, once inflation breaks over 5%, it takes an average of 10 years for it to drop back down to 2%.

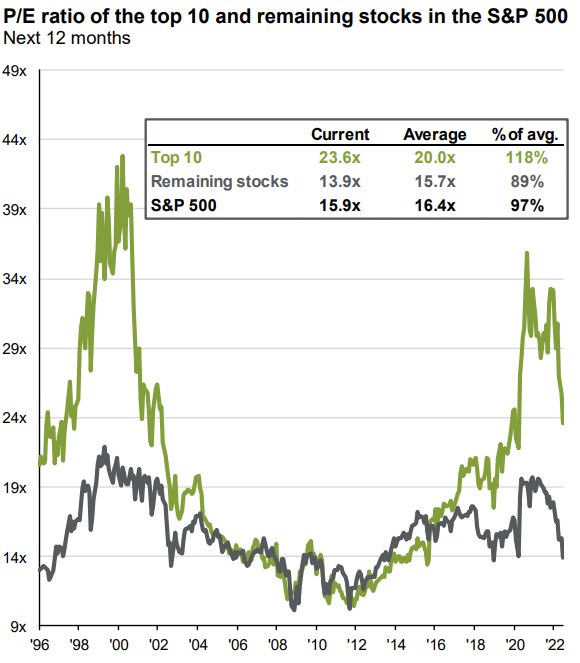

EXHIBIT 3 - biggest stocks still seeing high valuations

The views expressed above reflect the views of EdgeTech Analytics, LLC and are for informational purposes only. These views are not intended to serve as a substitute for personalized investment advice. Past performance is no guarantee of future results and no investment strategy or methodology can guarantee profits or protect against losses.