Powell’s Corrections of Market Misconceptions

INFLATION • THE FED • JEROME POWELL

The late summer stock market rally was fueled by the market’s misconception of the severity of inflation and the seriousness of the Fed’s determination to defeat it. Chairman Jerome Powell offered correctives to these misconceptions in his speech at Jackson Hole last week.

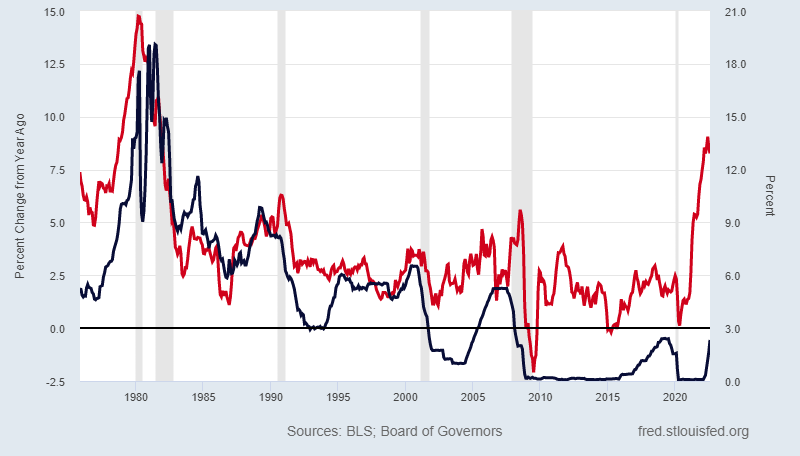

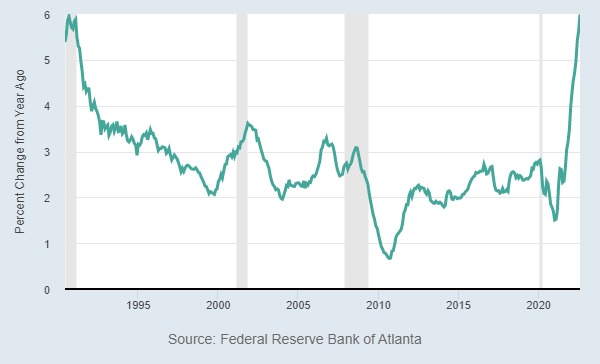

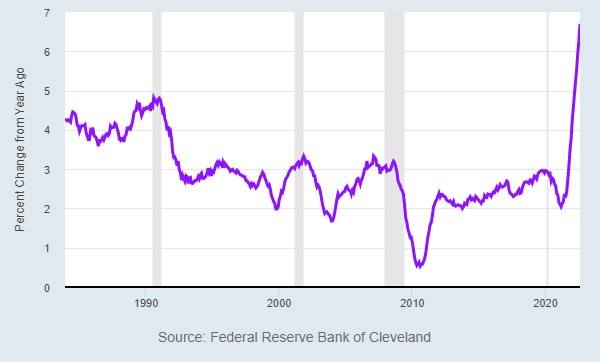

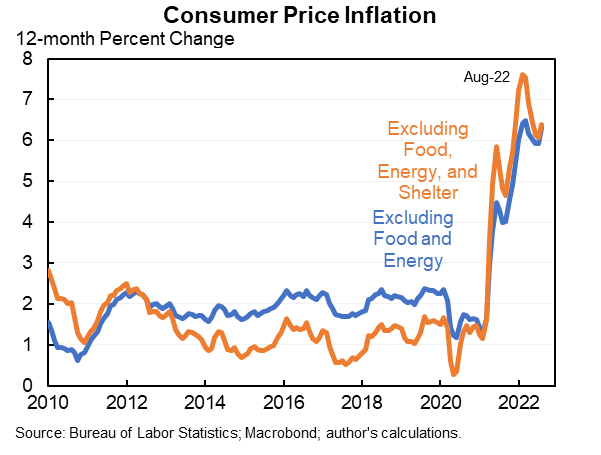

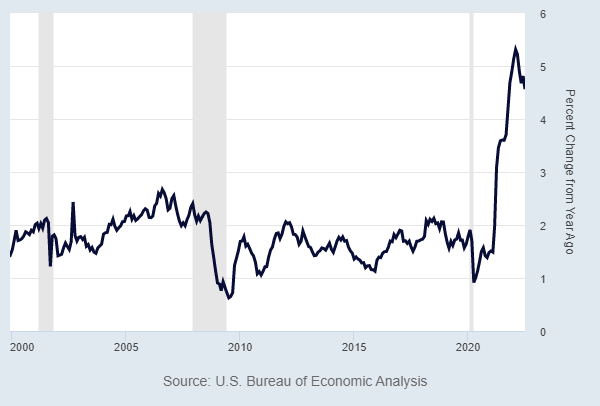

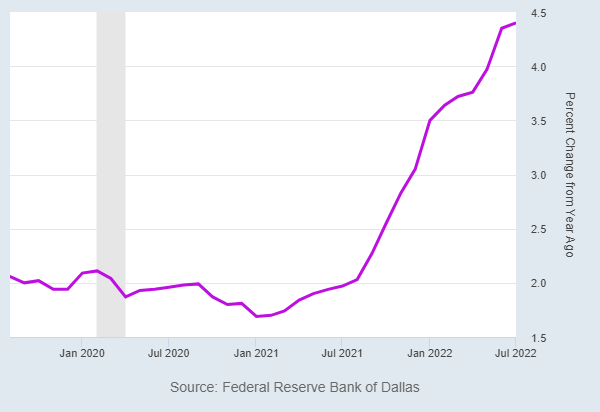

MISCONCEPTION #1: INFLATION’S PEAKED, NOT A BIG DEAL GOING FORWARD

- “High inflation has continued to spread through the economy.”

- “Without price stability, the economy does not work for anyone.”

- “Reducing inflation is likely to require a sustained period of below-trend growth.”

- “While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses.”

- “These are the unfortunate costs of reducing inflation. But a failure to restore price stability would mean far greater pain.”

MISCONCEPTION #2: THE FED WILL PIVOT AND REVERSE COURSE:

- “Restoring price stability will likely require maintaining a restrictive policy stance for some time.”

- “The historical record cautions strongly against prematurely loosening policy.”

- “We are taking forceful and rapid steps to moderate demand so that it comes into better alignment with supply, and to keep inflation expectations anchored. We will keep at it until we are confident the job is done.”

RESETTING EXPECTATIONS:

The market must reset its expectations and come to terms with the one-two punch of both inflation and interest rates that are going to be higher for longer.

The Fed’s commitment to taming inflation is going to slow the economy. This is their clearly stated goal.

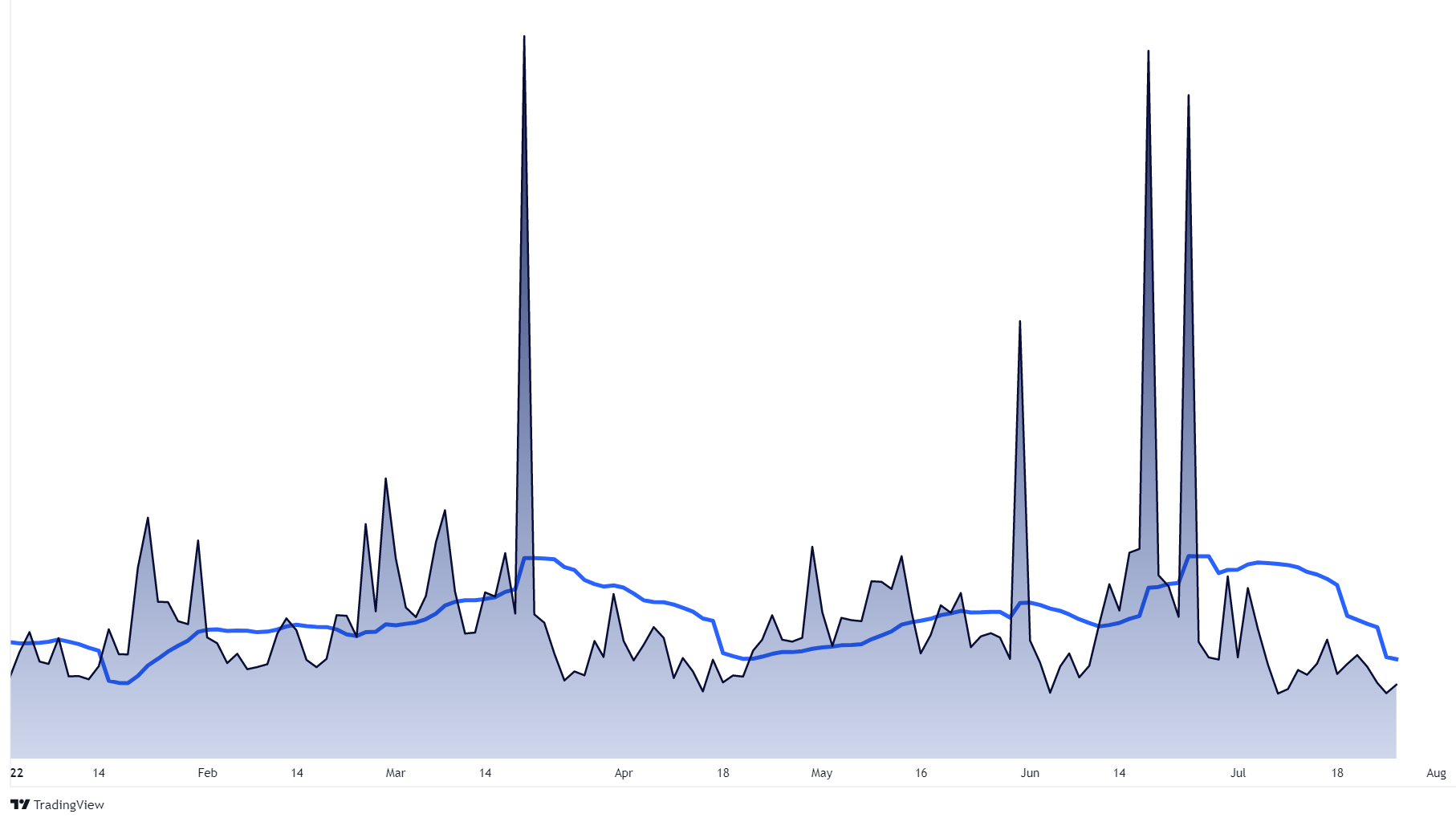

With the reset of expectations comes the return of erratic price swings as the stock market becomes more volatile in anticipation of the Fed’s goal coming to fruition.

Going forward stocks are going to have a hard time gaining traction in a stagflationary, rising interest rate environment.

- What explains the late-summer stock market rally that has already come to an abrupt end?

- We think the stock market deceived itself into thinking that the Federal Reserve would dial back its interest rate hikes in response to the assumed peak in inflation.

- The market misjudged both the severity of inflation and the seriousness of the Fed’s determination to defeat it.

This misjudgment was based on two things:

- The perceived dovishness of Chairman Jerome Powell, and

- Memories of the Fed’s quick reversal (aka “pivot”) of their rate hikes in 2019 in response to a similar stock market sell-off.

The difference this time is entrenched, elevated inflation.

- It is literally the Fed’s job to maintain stable prices.

- Since it became apparent that inflation isn’t transitory, the Fed has been absolutely clear about their intentions to stabilize prices regardless of the pain this will cause the economy and the stock market.

- And far from being the stock market’s backstop, the Fed has not minced words about its willingness to inflict pain in order to lower prices.

- As Chairman Powell stated last week, higher rates will, “bring some pain to households and businesses. But a failure to restore price stability would mean far greater pain.”

- Instead of a Fed pivot we got a Fed double down. They are resolved not to repeat their mistakes from the 1970s when they eased before inflation was dead and buried.

- They couldn’t be more clear that they will follow their mandate and hike interest rates until they are confident that inflation is moving down.

©2022 EdgeTech Analytics, LLC. All rights reserved. For informational purposes only. This is not an offer to buy or sell any securities. No investment strategy is free from risk and there is no guarantee that any strategies mentioned herein will be profitable. Past performance is not indicative of future performance.