The markets and the Fed now are in agreement on one thing: something will have to break in order to get inflation under control.

Today’s stock market reversal highlights this new parallel thinking:

The Fed is focused on the labor market and believes it must loosen (i.e., there needs to be higher unemployment) in order for prices finally to ease.

Weekly jobless claims came in today below expectations and have continued to fall steadily since July.

And so good economic news—more people have jobs—is bad market news because it means more rate hikes from the Fed.

The S&P 500 is set to fall to a new bottom today (it’s about -24% away from its peak).

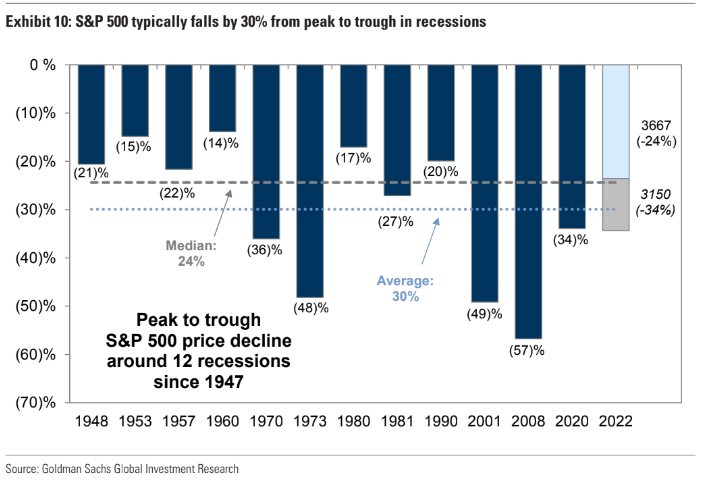

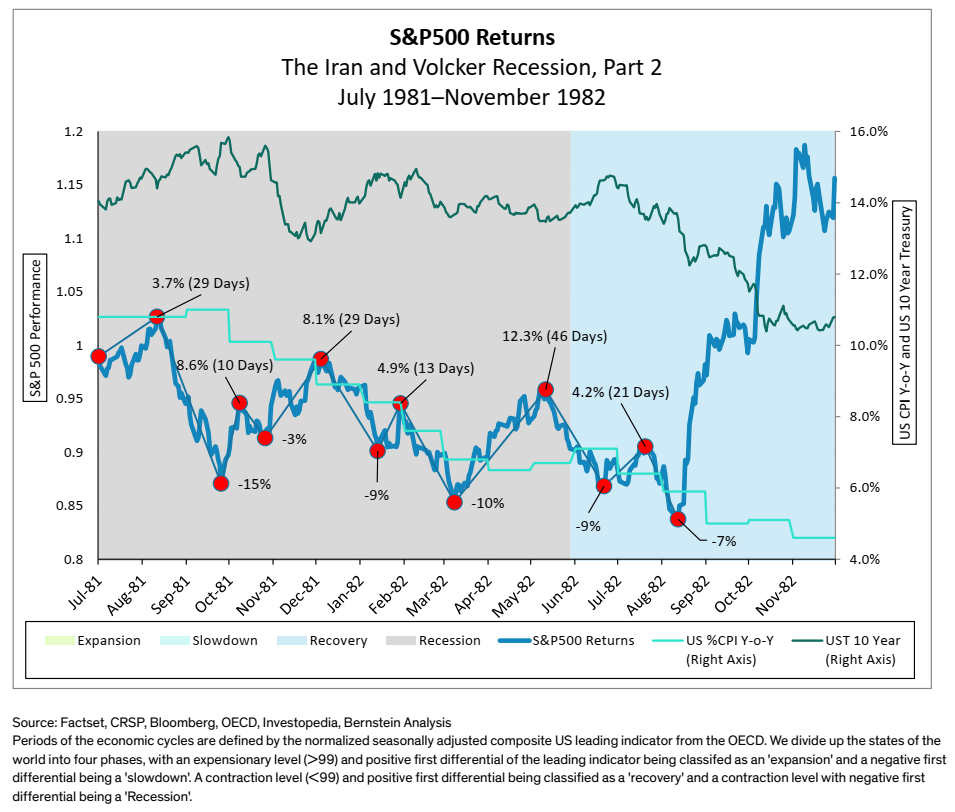

The average drawdown for the S&P 500 around recessions is -30%.

The headline index has closed negative 56% of its trade days so far this year. Since 1957 this is the index’s second-most negatively-biased year. The most negative year (in terms of closing negative) was 1974 when 58% of trade days were negative.

Just 15% of S&P 500 companies are trading above their 200-day moving average; just 7% are trading above their 50-day moving average.

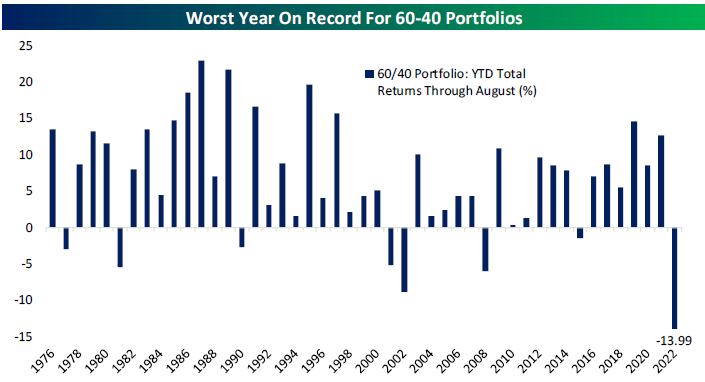

The Dow fell into a bear market for the first time since 2020. Both the Dow Industrials and Dow Transportation Averages are in bear markets. Long Treasuries are having their worst 1-year performance ever (they’re now down over -30% year-over-year). Including inflation to give us the real return, this is the worst performing year ever for the 60/40 portfolio.

The 60/40 is down -20% ytd. With inflation it’s down -27%, worse than 1974’s terrible real return of -25%.

KEY TAKEAWAYS

Good economic news is bad news for markets.

Volatility will persist into the next quarter in response to economic data and the upcoming earnings season.

The VIX is climbing and is elevated, but is not yet at extreme levels.

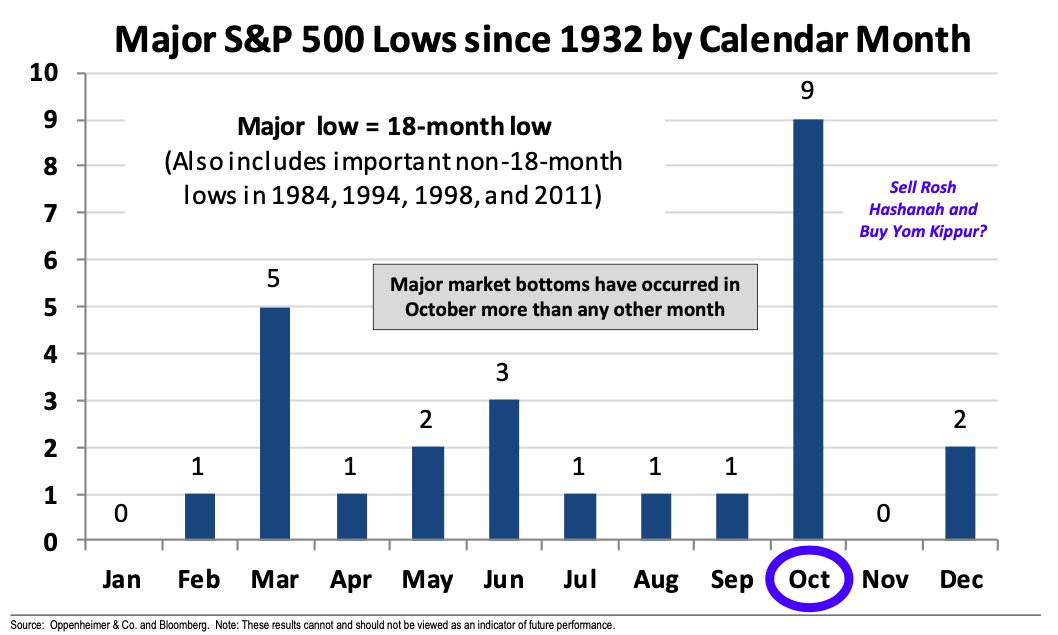

October is historically the market’s most volatile month.

More market bottoms have been reached in October than in any other month.

The tactical stance will be to preserve and protect in the face of ever more volatile markets. The software will be looking for durable trends should a firm bottom be put in. Catalysts are few and far between.

MARKET CHARTS

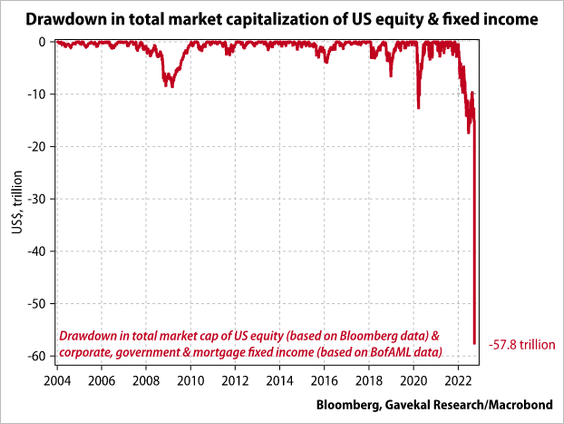

EXHIBIT 1 - this drawdown has been historic

This chart from Gavekal Research shows the total market cap lost to this year’s bear markets in stocks and bonds. The total comes to -$57.8 trillion capitalization shaved off so far this year.

EXHIBIT 2 - Volatile October, friend to finding the bottom

TITLE

Suspendisse lobortis diam molestie enim facilisis, eget malesuada sapien vestibulum. Suspendisse at sapien augue. Morbi ex felis, commodo a dui sit amet, ullamcorper bibendum elit.

EXHIBIT 3 - End of bull market in bonds?

We’ve seen this year a definite break in 35-year decline in bond yields. There have been breaks over previous highs before, but this most recent breakout is significantly larger than those others.

EXHIBIT 4 - S&P Averages -30% drawdown around recessions

We’ve seen this year a definite break in 35-year decline in bond yields. There have been breaks over previous highs before, but this most recent breakout is significantly larger than those others.

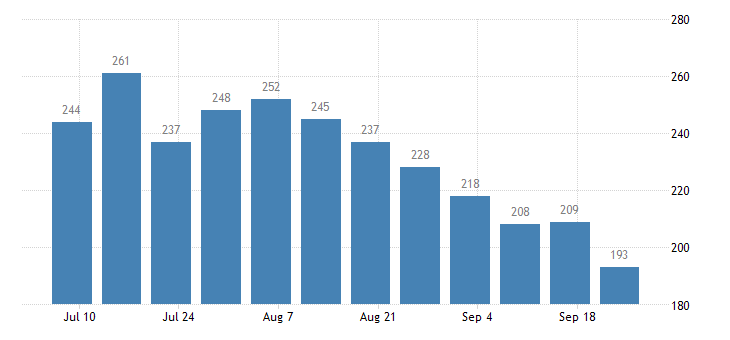

EXHIBIT 5 - initial jobless claims

Needless to say, this is not what the Fed wants to see from the labor market in their quest to kill inflation.

Such data will reinforce the Fed’s stated decision to double-down and continue to attack inflation quickly and forcefully.

The views expressed above reflect the views of EdgeTech Analytics, LLC and are for informational purposes only. These views are not intended to serve as a substitute for personalized investment advice. Past performance is no guarantee of future results and no investment strategy or methodology can guarantee profits or protect against losses.

The stock market is now confronting the unavoidable: entrenched inflation and a Fed Chairman ready and willing to be the next Paul Volcker.

In this unusual post-pandemic macro environment the Fed’s dual mandate—full employment and stable prices—are in direct conflict.

With the employment rate at just 3.7% the Fed has made the correct judgment call that defeating inflation should be their primary focus for the foreseeable future.

As Chairman Powell stated, a failure to tame inflation with current economic pain would only lead to far greater pain in the future.

And so stocks have seen extreme volatility and have sold off about -10% since the Jackson Hole speech.

Stocks sold off on yesterday’s 75 basis point hike and Powell’s hawkish comments in his afternoon press conference. Some choice quotes:

“It would be nice if there was a way to just wish it [inflation] away, but there isn’t.”

“We think we need to have softer labor market conditions.” I.e., the Fed is willing to tolerate higher unemployment.

“We have got to get inflation behind us. I wish there were a painless way to do that; there isn’t.”

The S&P has again fallen -20% from its peak and the Nasdaq has again fallen -30% from its peak. Both last saw these low levels in July before the summer bear market rally.

Just 15% of S&P 500 stocks are trading above their 50-day moving average; just 10% of Nasdaq 100 stocks are.

KEY TAKEAWAYS

The Fed seems to have given up hope of a “soft landing” and admit economic pain will likely be a necessity to bring inflation down.

Rates are going to continue higher until the Fed sees “compelling” evidence that inflation is moving in the right direction.

What consitutes “compelling” we can’t know, but this uncertainty ushers in volatility in anticipation of every inflation-related data release.

Also, the certainty of higher rates ensures the continued presence of a massive headwind for stock prices.

Such erratic markets facing certain, known headwinds makes for an extremely difficult trading environment. Tactical, defensive allocations to cash and cash-like instruments will be helpful in avoiding catching a knife that’s both falling and bouncing around.

MARKET CHARTS

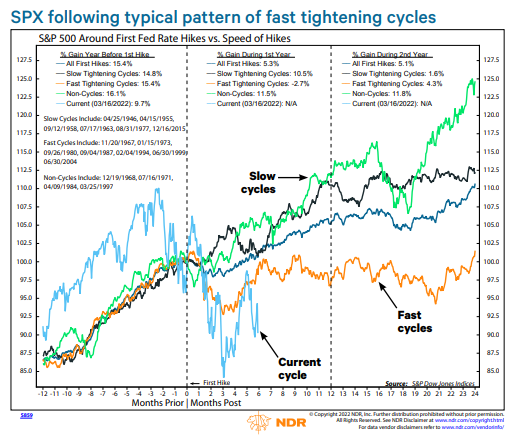

EXHIBIT 1 - Fast rate-tightening cycles leads to disappointing returns

This chart from Ned Davis Research shows S&P 500 performance during different speed rate-tightening cycles.

Fast hiking/tightening leads to volatile, flat performance historically.

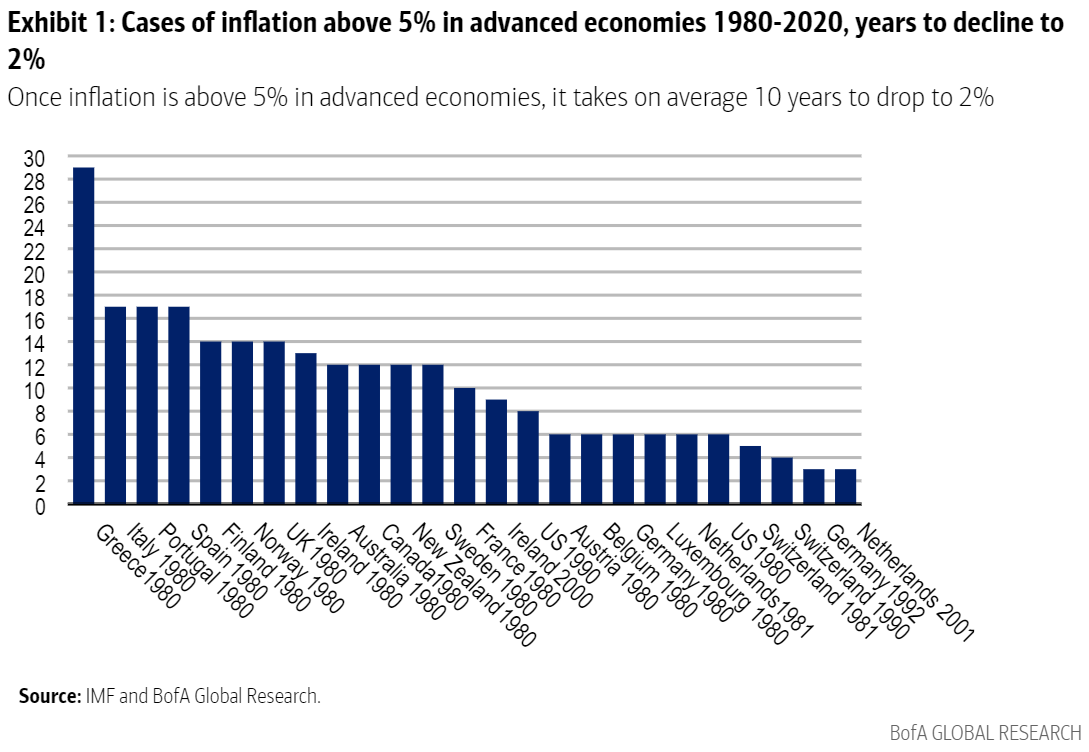

EXHIBIT 2 - how long to kill inflation?

Research from Bank of America shows that in advanced economies, once inflation breaks over 5%, it takes an average of 10 years for it to drop back down to 2%.

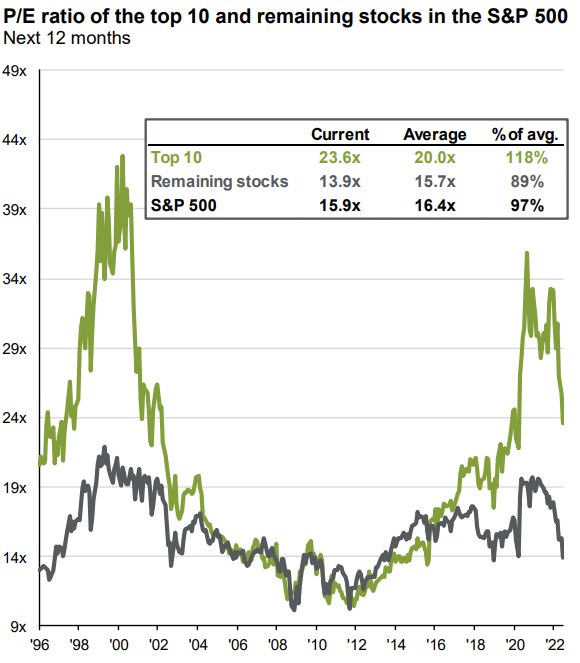

EXHIBIT 3 - biggest stocks still seeing high valuations

The views expressed above reflect the views of EdgeTech Analytics, LLC and are for informational purposes only. These views are not intended to serve as a substitute for personalized investment advice. Past performance is no guarantee of future results and no investment strategy or methodology can guarantee profits or protect against losses.

The late summer stock market rally was fueled by the market’s misconception of the severity of inflation and the seriousness of the Fed’s determination to defeat it. Chairman Jerome Powell offered correctives to these misconceptions in his speech at Jackson Hole last week.

MISCONCEPTION #1: INFLATION’S PEAKED, NOT A BIG DEAL GOING FORWARD

“High inflation has continued to spread through the economy.”

“Without price stability, the economy does not work for anyone.”

“Reducing inflation is likely to require a sustained period of below-trend growth.”

“While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses.”

“These are the unfortunate costs of reducing inflation. But a failure to restore price stability would mean far greater pain.”

MISCONCEPTION #2: THE FED WILL PIVOT AND REVERSE COURSE:

“Restoring price stability will likely require maintaining a restrictive policy stance for some time.”

“The historical record cautions strongly against prematurely loosening policy.”

“We are taking forceful and rapid steps to moderate demand so that it comes into better alignment with supply, and to keep inflation expectations anchored. We will keep at it until we are confident the job is done.”

RESETTING EXPECTATIONS:

The market must reset its expectations and come to terms with the one-two punch of both inflation and interest rates that are going to be higher for longer.

The Fed’s commitment to taming inflation is going to slow the economy. This is their clearly stated goal.

With the reset of expectations comes the return of erratic price swings as the stock market becomes more volatile in anticipation of the Fed’s goal coming to fruition.

Going forward stocks are going to have a hard time gaining traction in a stagflationary, rising interest rate environment.

What explains the late-summer stock market rally that has already come to an abrupt end?

We think the stock market deceived itself into thinking that the Federal Reserve would dial back its interest rate hikes in response to the assumed peak in inflation.

The market misjudged both the severity of inflation and the seriousness of the Fed’s determination to defeat it.

This misjudgment was based on two things:

The perceived dovishness of Chairman Jerome Powell, and

Memories of the Fed’s quick reversal (aka “pivot”) of their rate hikes in 2019 in response to a similar stock market sell-off.

The difference this time is entrenched, elevated inflation.

It is literally the Fed’s job to maintain stable prices.

Since it became apparent that inflation isn’t transitory, the Fed has been absolutely clear about their intentions to stabilize prices regardless of the pain this will cause the economy and the stock market.

And far from being the stock market’s backstop, the Fed has not minced words about its willingness to inflict pain in order to lower prices.

As Chairman Powell stated last week, higher rates will, “bring some pain to households and businesses. But a failure to restore price stability would mean far greater pain.”

Instead of a Fed pivot we got a Fed double down. They areresolved not to repeat their mistakes from the 1970s when they eased before inflation was dead and buried.

They couldn’t be more clear that they will follow their mandate and hike interest rates until they are confident that inflation is moving down.

The keyword for markets going forward is instability.

Following Tuesday’s unexpectedly higher CPI numbers, the market has been forced to abandon its hope for a quick end to inflation and a Fed pivot.

Instead markets must confront the following:

Inflation that is going to be higher for longer.

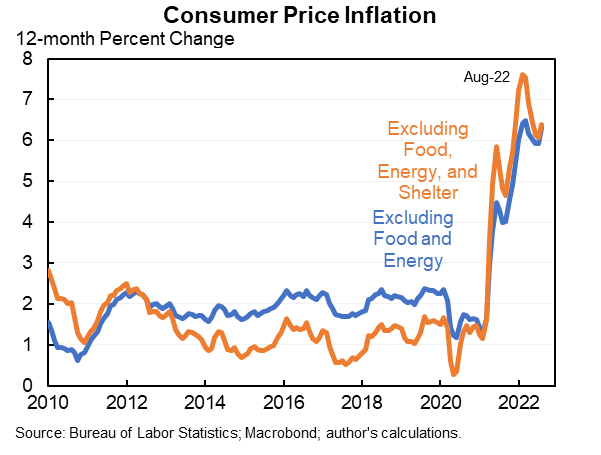

Most tellingly, the inflation measures most representative of entrenched inflation (Core CPI, Median and Trimmed Mean CPI, and Sticky CPI) are not showing any signs of slowing down (see charts below).

Outside of gasoline, food prices affect consumers most and food prices are not moderating. Food inflation was up +11.5% and grocery inflation is running at +13.5% year-over-year (highest since 1979).

A Federal Reserve that is laser-focused on defeating inflation.

The Fed is not going to pivot anytime soon.

As Chairman Powell stated at Jackson Hole, they are willing to take “forceful and rapid steps to moderate demand.”

Higher interest rates until prices moderate enough to satisfy the Fed.

More rate hikes are on the way as the terminal Fed Funds rate may need to be even higher in order to effectively curb demand (see chart below).

Slower demand means a slowing economy means reduced earnings.

A recession may be needed to stop stubborn inflation.

Investors must be prepared for such a recession/slowdown to show up in a company’s bottom lines.

This makes for an unstable, uncertain market.

There are few catalysts to buy when the market is staring down the barrel of the inevitable: a forced economic contraction that might, we hope, stabilize prices.

KEY TAKEAWAYS

Slowdown arriving soon? Atlanta Fed’s most recent estimate for Q3 GDP growth falls to 0.5%.

The certainties for this economy (higher rates, falling demand) make for an uncertain stock market.

Uncertainty for stocks means volatility.

Further whipsaws, bear market rallies, and high magnitude intra and interday moves are to be expected in the coming months.

We are seeing further defensive tactical allocations to cash and cash-like instruments as a way to approach this trendless market.

MARKET CHARTS

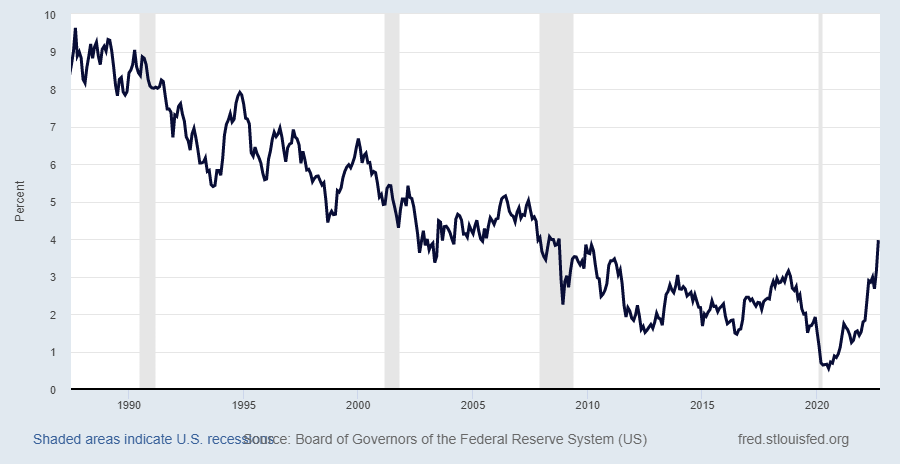

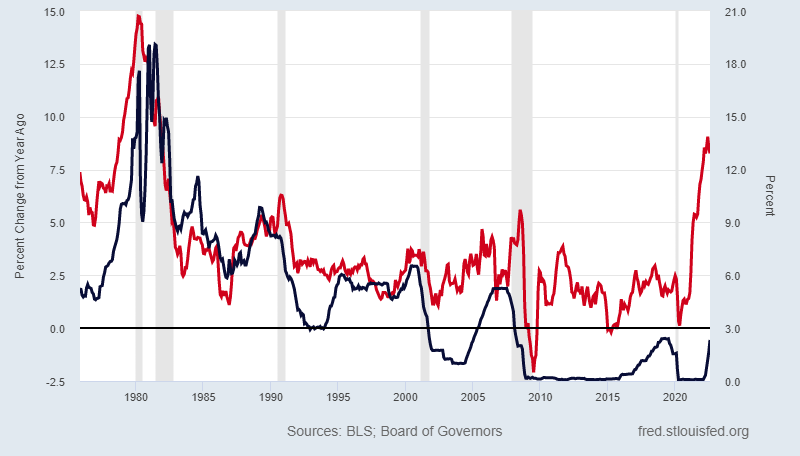

EXHIBIT 1 - Inflation and the fed funds rate

Here we see the rate of inflation (red line) and the effective Fed Funds Rate (blue line). Hiking the Fed Funds Rate is a key part of how the Fed is trying to bring inflation down.

You can see how low the rate remains even after the hikes so far this year. Does this imply the rate needs to be much higher to pull inflation down?

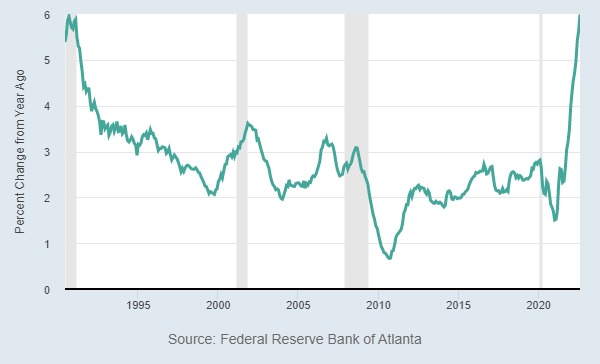

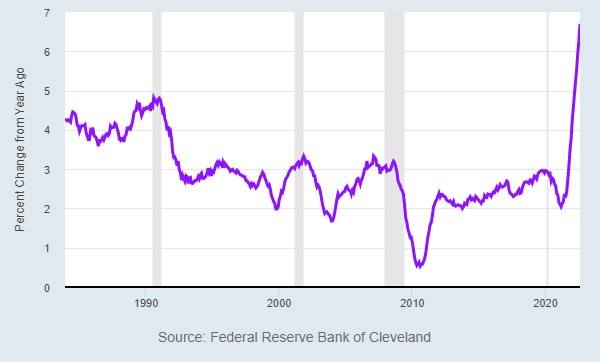

EXHIBIT 2 - fed isn’t budging from being “forceful and rapid” in their hikes

Sticky CPI: highest since ’82, no signs of slowing down.

Median CPI: highest ever recorded (index started in ’83), not slowing.

Core Core CPI: excludes food, energy and shelter, still above 6%.

EXHIBIT 3 - Stock returns and last inflationary regime

During our last bout of elevated inflation and rising interest rates stocks didn’t bottom until over two years after the peak in inflation. In between? Sideways movement with whipsaws and bear market rallies.

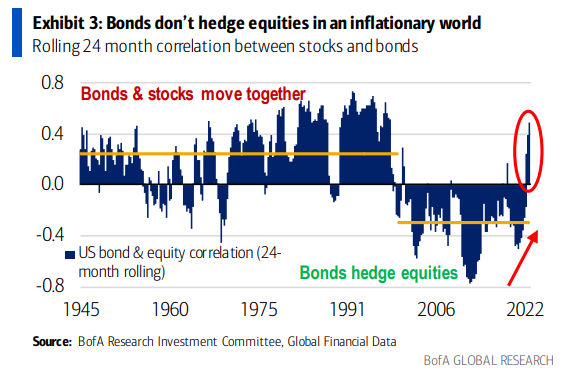

EXHIBIT 4 - bonds don't hedge equities in inflationary world

The views expressed above reflect the views of EdgeTech Analytics, LLC and are for informational purposes only. These views are not intended to serve as a substitute for personalized investment advice. Past performance is no guarantee of future results and no investment strategy or methodology can guarantee profits or protect against losses.

Conflicting economic data this week only added to the general confused, unstable direction of markets.

The ISM Services PMI came in over expectations, increasing month-to-month, and in expansionary territory. The ISM Manufacturing PMI also came in over expectations staying flat in August.

Neither index is indicating recession and both continue to show steadily falling prices (good news for inflation).

Regardless, the Fed has made clear that further rate hikes are a certainty. The questions facing investors now are:

Will the Fed break something in its quest to quash inflation?

If it does, what will it break?

Look for deterioration in the housing market (definitely in a correction; still a ways to go to get back to normal), labor market (showing significant strength; few signs of loosening), broad economic demand (GDP), or the stock market (lower lows; lower multiples).

Is a soft landing possible?

Again the labor market is showing continued strength (jobless claims have fallen for 4 straight weeks; see also increased participation numbers from last week’s Talking Points), and manufacturing and services indexes continue to show expansionary levels with falling prices.

Stocks remain under pressure.

The S&P 500 remains down -17% from its peak.

The index has traded below its 200-day moving average for over 100 trade days. This is the longest streak since the Great Financial Crisis (2009).

The Nasdaq remains down -26% from its peak.

Like the S&P, the Nasdaq has traded below its 200-day moving average for over 100 trade days; also the index’s longest streak since 2009.

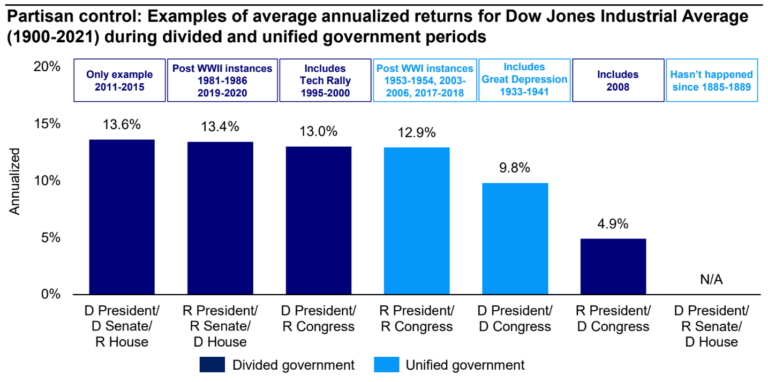

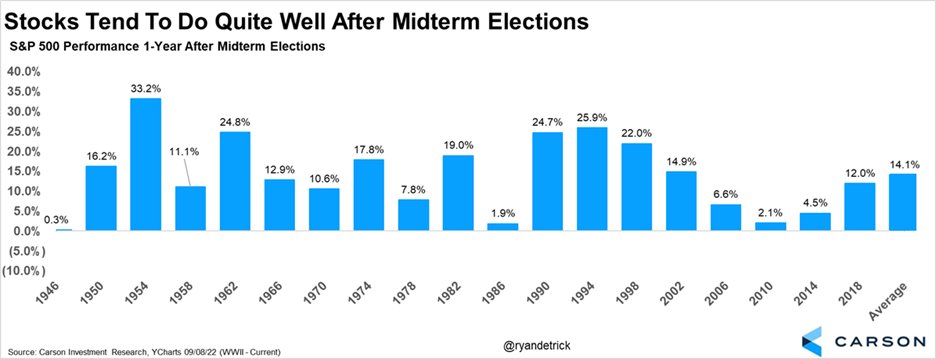

ELECTIONS APPROACHING

MARKETS LIKE DIVIDED GOVERNMENT, POST-MIDTERM YEARS

MARKET CHARTS

EXHIBIT 1 - aggregate bond index off to its worst-ever start

The AGG’s inception was 1976, before the runaway inflation of 1979-1980, and this year remains far and away the index’s worst start ever.

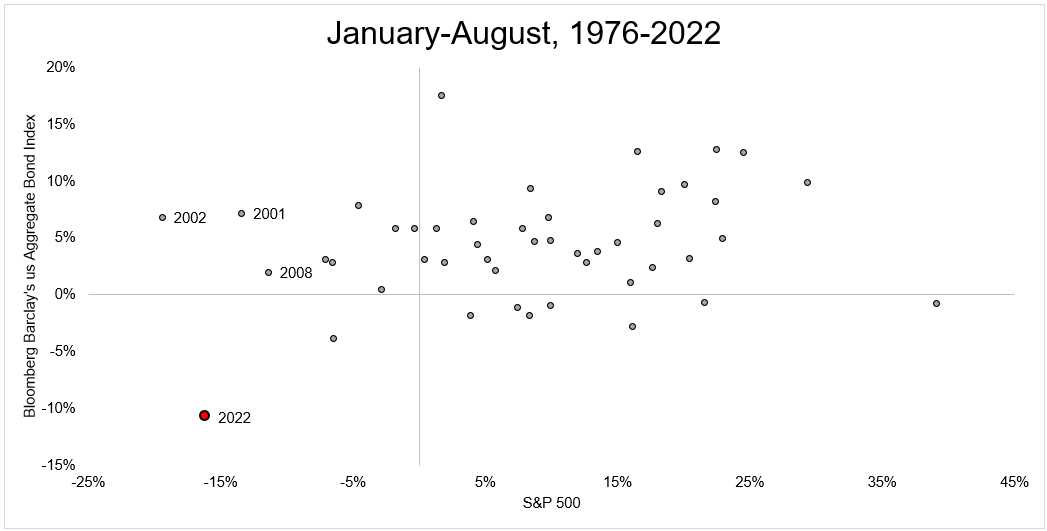

EXHIBIT 2 - 60/40 portfolio’s worst year on record

The chart below left, from Michael Batnick, charts the S&P 500 returns on the horizontal axis and the Aggregate bond return on the vertical axis. You can see that 2022 is in a league of its own.

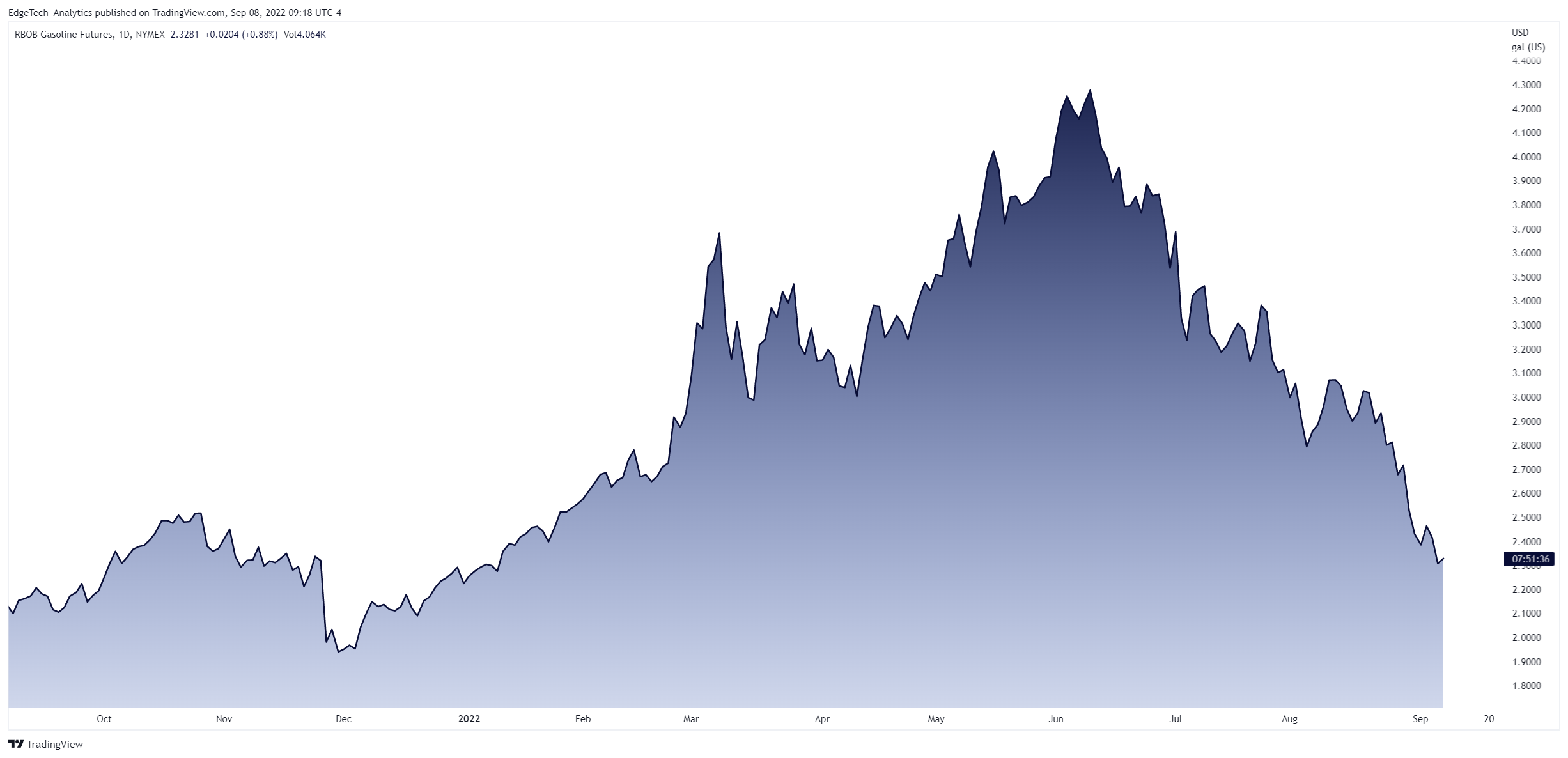

Gasoline futures currently at $2.30…should translate to $3.15/gallon in about a month. The broad basket commodities index ETF, DBC, fell below its 200-day moving average for the first time since October of 2020.

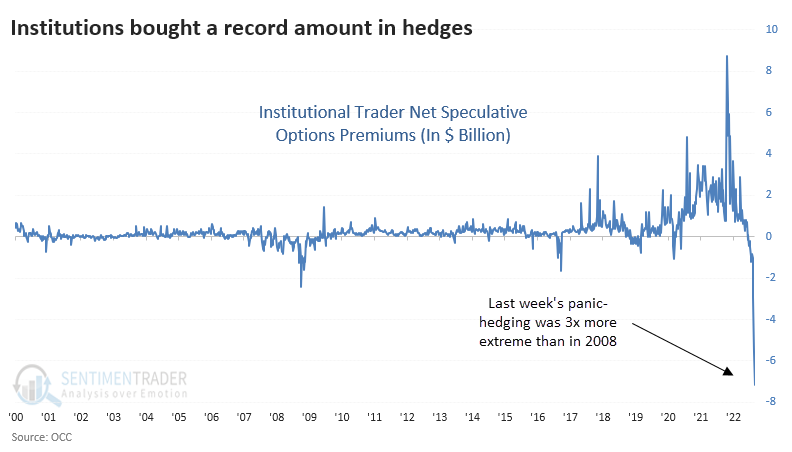

EXHIBIT 4 - Institutions buying protection

Institutional traders bought record amounts of put options, hedging their positions to protect on anticipated downdrafts.

The views expressed above reflect the views of EdgeTech Analytics, LLC and are for informational purposes only. These views are not intended to serve as a substitute for personalized investment advice. Past performance is no guarantee of future results and no investment strategy or methodology can guarantee profits or protect against losses.